Review of Operations

Note: This section covers business results for the head office only, with gross written premiums used to measure business volume and the combined ratio calculated under IFRS 4.

Note: This section covers business results for the head office only, with gross written premiums used to measure business volume and the combined ratio calculated under IFRS 4.

UY2025 closed with results exceeding our bottom-line targets. Gross written premiums slightly increased from KRW 167.5 billion in 2024 to KRW 180.9 billion in 2025. This growth was driven by a steady flow of new accounts written across all lines of business, as we continued to explore opportunities in untapped markets. Throughout the year, our disciplined and conservative underwriting philosophy remained central to preserving profitability amid evolving market conditions.

Our underwriting (U/W) guidelines for 2026 will stay unchanged, as our priority continues to be on bottom-line performance. We refine our U/W discipline through risk selection, line size management, analysis of discrepancies between actual premium rates and technical rates, and the application of coverage restrictions. We will consistently take a conservative approach toward high-hazardous occupancies, as well as risks vulnerable to inflation and economic cycles, including those with high business interruption exposure.

Over the years, we have improved our underwriting approach to better reflect regional market dynamics and local client expectations. This adaptive approach has enhanced our ability to access new opportunities. In particular, North America has remained a key growth region, where pricing has been comparatively resilient and demand for facultative capacity has been robust, even as broader market conditions have softened.

We have also made tangible progress toward achieving a more geographically balanced portfolio. Exposure in Asia has gradually moderated, while North America has increased its relative contribution, supporting diversification and reducing regional concentration risk.

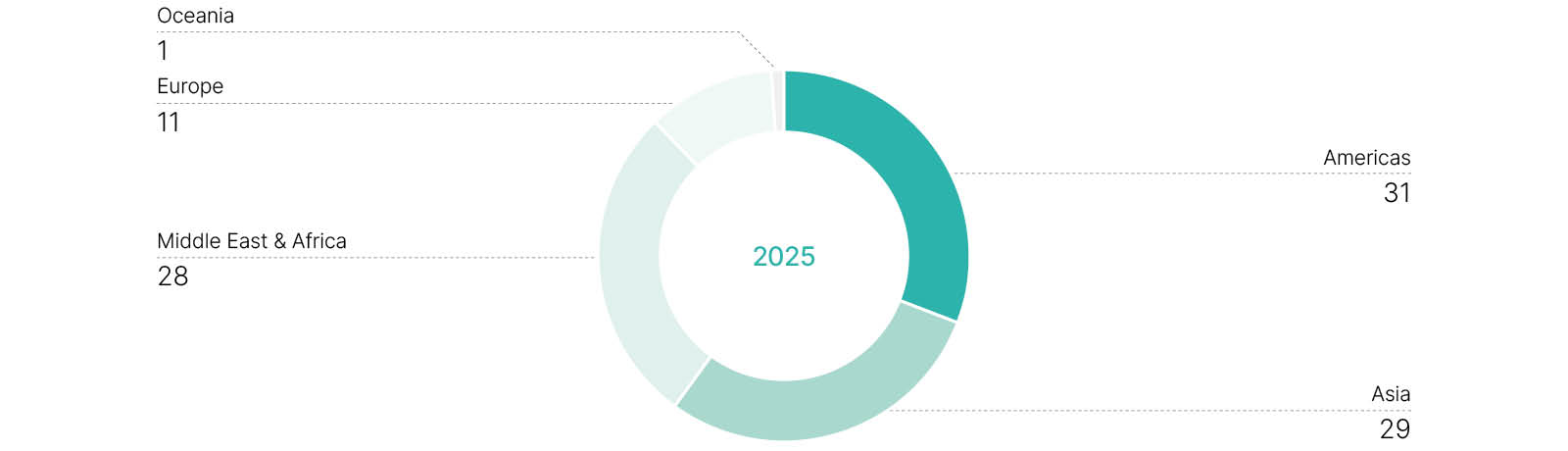

Our premium breakdown by territory is illustrated below, with Asia and MEA together accounting for more than half of total premium income, followed by the Americas (31%), Europe (11%), and Oceania (1%). Given the relatively modest exposure of Europe within our current portfolio, we plan to expand our exposure in Europe through new business opportunities from 2026 onward.

The favorable pricing momentum that previously supported both growth and profitability has largely transitioned into a softer market phase.

Looking ahead, we recognize that ongoing uncertainties driven by large-scale catastrophe losses and an increasingly competitive environment amid ongoing market softening will present challenges to achieving our objectives. Nevertheless, we remain confident in our ability to navigate these conditions by adhering to disciplined underwriting principles and by consistently providing our clients with technical expertise and reliable capacity. Through a balanced approach combining outward retrocession strategies and prudent risk retention, we aim to sustain a consistently profitable portfolio despite increasingly competitive market conditions. These core strengths have long underpinned our performance and will remain fundamental to the sustainable, long-term development of our facultative portfolio.

(Unit: %)

(Units: KRW billion, USD million)

| 2025 (KRW) | 2025 (USD) | 2024 (KRW) | 2024 (USD) | |

| International Property Facultative | 180.9 | 126.1 | 167.5 | 122.4 |

Korean Re’s international engineering & construction business continues to operate under a profitability-driven underwriting strategy. We have further strengthened our underwriting discipline with portfolio optimization at its core, consistently prioritizing risk selection and in-depth technical analysis. Although market conditions have gradually shifted toward a softer phase amid increasing competition, we remain firmly committed to a quality-over-volume approach. Through this disciplined strategy, we aim to secure sustainable and resilient long-term profitability.

The global construction market has broadly entered a phase of stabilization, though the pace of investment activities varies by region and sector. In several advanced economies, private investment in housing and industrial sectors is gradually recovering alongside a steady pipeline of public projects. Meanwhile, emerging economies continue to promote large-scale, government-led infrastructure projects. In particular, AI-related infrastructure—including data centers, power grid expansion, and energy storage facilities—is expected to sustain mid- to long-term growth momentum, driven by structural demand.

In the energy sector, investments in energy transition are increasingly being pursued in parallel with conventional power generation and natural resource development projects aimed at enhancing energy security and supply chain stability. This dual-track investment dynamic is accelerating diversification within the global energy portfolio and providing a stable demand base for construction activities.

At the same time, volatility in natural catastrophe losses and ongoing geopolitical uncertainties continue to shape the global project risk landscape. As a result, accumulation control and natural catastrophe exposure analysis have become increasingly important, and we have embedded these disciplines as core elements of our portfolio management framework.

In 2026, we will continue to pursue sustainable and profitable growth through rigorous risk selection and proactive portfolio management, supported by early detection of loss ratio deterioration indicators. We will also further strengthen collaboration among our claims specialists, risk engineers, and underwriters to enhance our integrated risk management capabilities. Amid a continuously evolving market environment, we will maintain consistent underwriting principles while delivering stable and reliable risk transfer solutions, thereby reinforcing our long-term competitiveness in the global market.

(Units: KRW billion, USD million)

| 2025 (KRW) | 2025 (USD) | 2024 (KRW) | 2024 (USD) | |

| International Engineering & Construction Facultative | 85.4 | 59.5 | 85.2 | 62.3 |

The global marine and energy insurance markets experienced another year of competitive pressure in 2025 amid abundant capacity and prolonged rate softening. While global maritime trade remained resilient, intensified competition exerted downward pressure on pricing across most hull & machinery and upstream energy classes. Insurers continued to compete aggressively for well-managed accounts, leading to sharper rate reductions in some segments. Despite this competitive landscape, the market remained vulnerable to volatility stemming from casualty events and inflation-driven increases in repair costs. Consequently, insurers prioritized risk differentiation based on risk management quality, loss records, and geopolitical exposure.

Against this backdrop, we strengthened our client-focused marketing efforts with a view to ensuring the retention of high-quality marine and energy accounts, while also selectively pursuing new opportunities to enhance portfolio diversification. We remained steadfast in our underwriting discipline, deliberately reducing participation in inadequately priced or volatility-prone risks. These reductions were successfully offset by selective growth in the fast-growing offshore wind and renewable energy sectors, as well as the stable retention of core blue-chip accounts.

As a result of these strategic initiatives, gross written premiums reached KRW 91.6 billion in 2025, representing a 17.4% year-on-year increase. Our focus on disciplined risk selection and portfolio optimization significantly improved the profitability of the marine & energy business, with a technical profit of approximately KRW 25.8 billion (before management expenses), a remarkable 124% increase from the previous year. Ongoing re-underwriting of underperforming sub-classes and proactive claims management played a pivotal role in consistently delivering underwriting profits.

As we enter 2026, we expect the international marine and upstream energy markets to remain competitive, with limited prospects for material rate hardening, absent major loss events. In response, we will continue to emphasize underwriting discipline and signed line protection, while accelerating our expansion into the energy transition and renewable sectors. By integrating technical risk engineering insights and optimizing the balance between conventional marine & energy risks and green energy projects, we aim to achieve sustainable growth while preserving long-term underwriting profitability.

(Units: KRW billion, USD million)

| 2025 (KRW) | 2025 (USD) | 2024 (KRW) | 2024 (USD) | |

| International Marine & Energy Facultative | 91.6 | 63.9 | 78.0 | 57.0 |